ISLR习题:线性回归 - 共线性问题

目录

本文源自《统计学习导论:基于R语言应用》(ISLR) 第三章习题

创建一组有共线性关系的数据集

set.seed(1)

x1 <- runif(100)

x2 <- 0.5 + x1 + rnorm(100) / 10

y <- 2 + 2 * x1 + 0.3 * x2 + rnorm(100)

$$ y = 2 + 2x_1 + 0.3x_2 $$

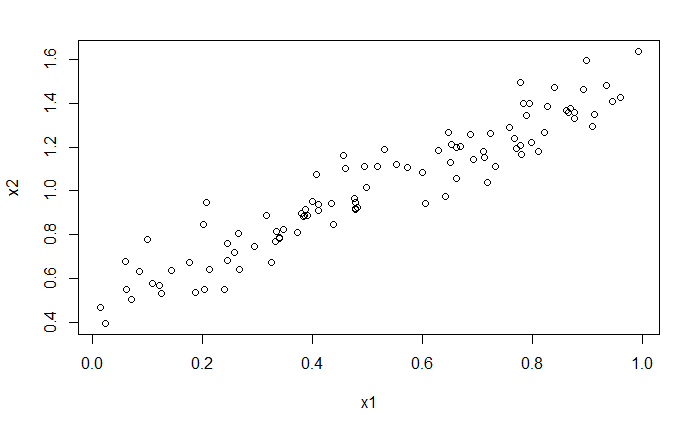

相关性

cor(x1, x2)

[1] 0.9469723

plot(x1, x2)

拟合

lm_fit_v1 <- lm(y ~ x1 + x2)

summary(lm_fit_v1)

Call:

lm(formula = y ~ x1 + x2)

Residuals:

Min 1Q Median 3Q Max

-2.8311 -0.7273 -0.0537 0.6338 2.3359

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.7757 0.5933 2.993 0.00351 **

x1 1.0847 1.2346 0.879 0.38179

x2 1.0097 1.1337 0.891 0.37536

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.056 on 97 degrees of freedom

Multiple R-squared: 0.2333, Adjusted R-squared: 0.2175

F-statistic: 14.76 on 2 and 97 DF, p-value: 2.54e-06

预测的 beta_1 和 beta_2 与真实值相差过大

x1 和 x2 系数的 p 值过小,不能拒绝零假设

单变量拟合

y 对 x1

lm_fit_x1 <- lm(y ~ x1)

summary(lm_fit_x1)

Call:

lm(formula = y ~ x1)

Residuals:

Min 1Q Median 3Q Max

-2.89495 -0.66874 -0.07785 0.59221 2.45560

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.2624 0.2307 9.805 3.21e-16 ***

x1 2.1259 0.3963 5.365 5.42e-07 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.055 on 98 degrees of freedom

Multiple R-squared: 0.227, Adjusted R-squared: 0.2191

F-statistic: 28.78 on 1 and 98 DF, p-value: 5.42e-07

p 值几乎为 0,可以拒绝零假设

y 对 x2

lm_fit_x2 <- lm(y ~ x2)

summary(lm_fit_x2)

Call:

lm(formula = y ~ x2)

Residuals:

Min 1Q Median 3Q Max

-2.74970 -0.68815 -0.03074 0.66090 2.34837

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.3789 0.3845 3.587 0.000525 ***

x2 1.9529 0.3639 5.367 5.36e-07 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.055 on 98 degrees of freedom

Multiple R-squared: 0.2272, Adjusted R-squared: 0.2193

F-statistic: 28.81 on 1 and 98 DF, p-value: 5.361e-07

p 值几乎为 0,可以拒绝零假设

错误观测

x1 <- c(x1, 0.1)

x2 <- c(x2, 0.8)

y <- c(y, 6)

多变量

y 对 x1 和 x2

lm_fit_v2 <- lm(y ~ x1 + x2)

summary(lm_fit_v2)

Call:

lm(formula = y ~ x1 + x2)

Residuals:

Min 1Q Median 3Q Max

-2.77906 -0.72031 -0.05796 0.62800 3.04112

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.5360 0.6115 2.512 0.0136 *

x1 0.1292 1.2407 0.104 0.9173

x2 1.7624 1.1500 1.532 0.1286

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.099 on 98 degrees of freedom

Multiple R-squared: 0.201, Adjusted R-squared: 0.1847

F-statistic: 12.32 on 2 and 98 DF, p-value: 1.682e-05

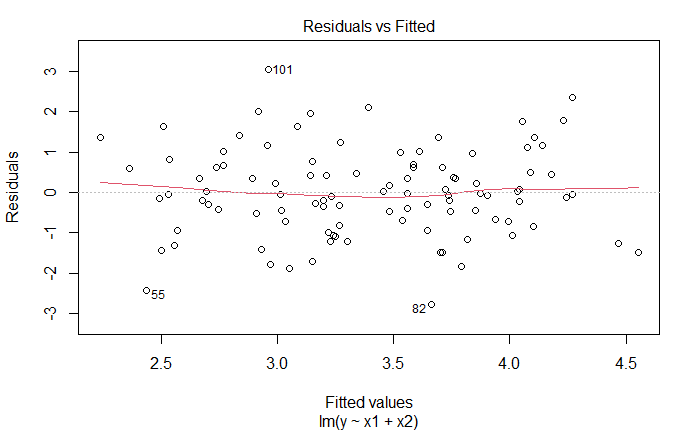

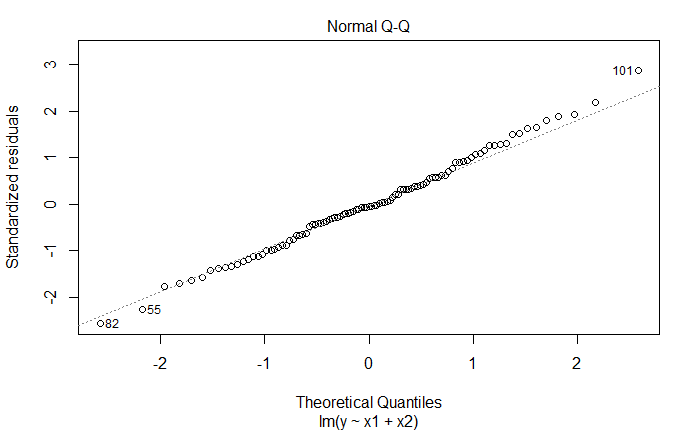

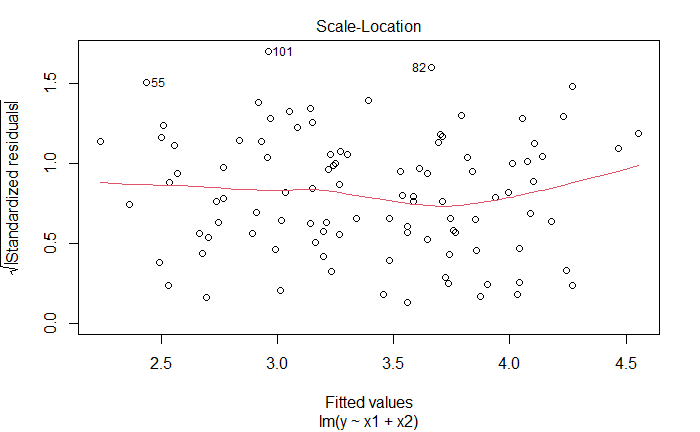

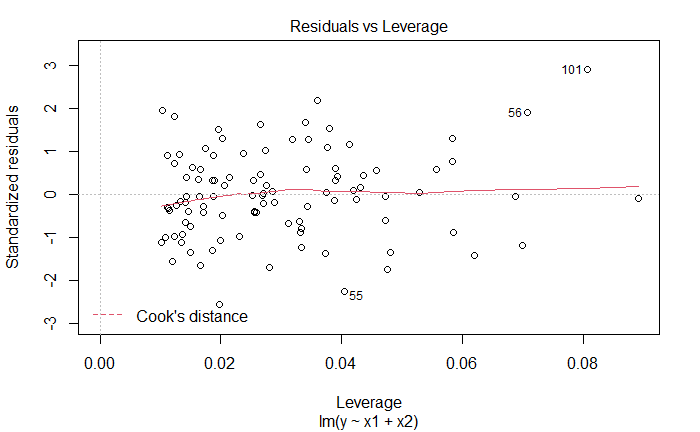

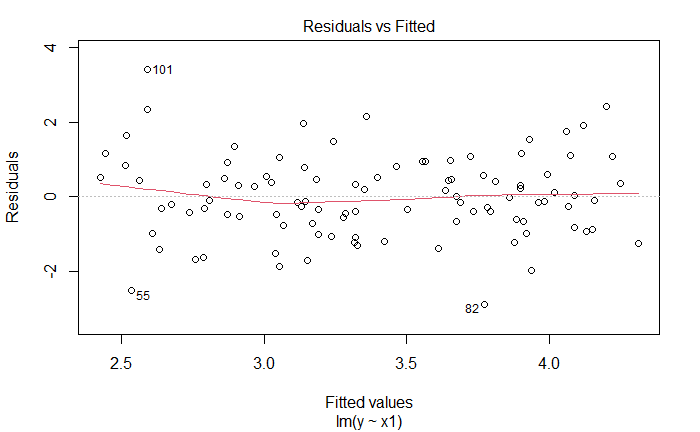

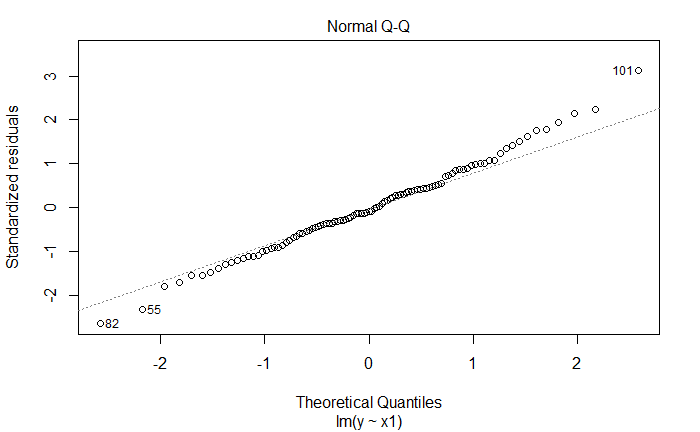

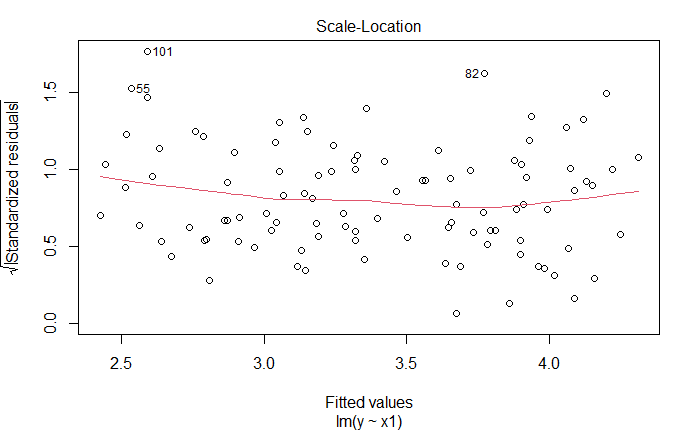

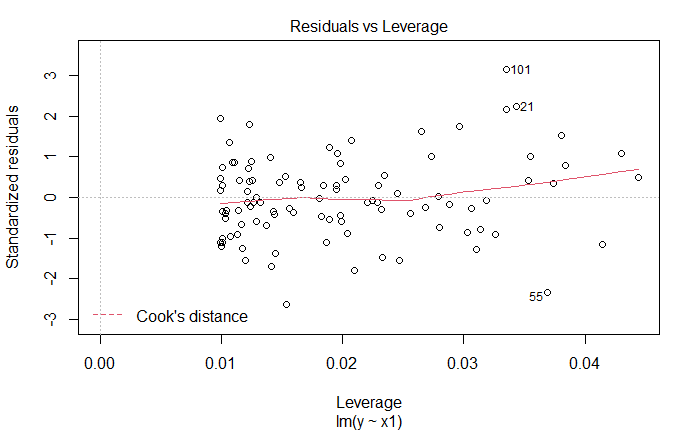

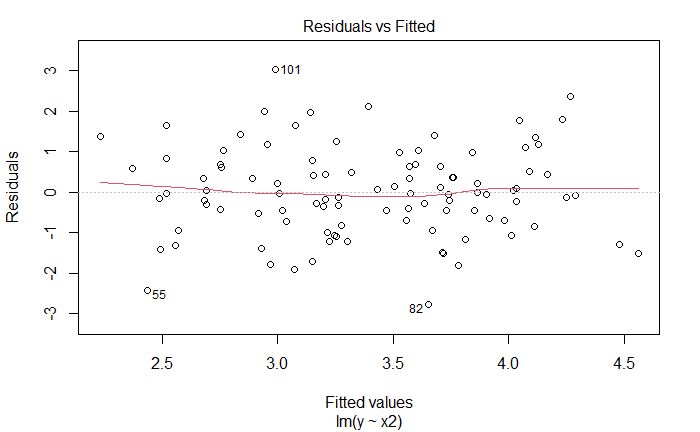

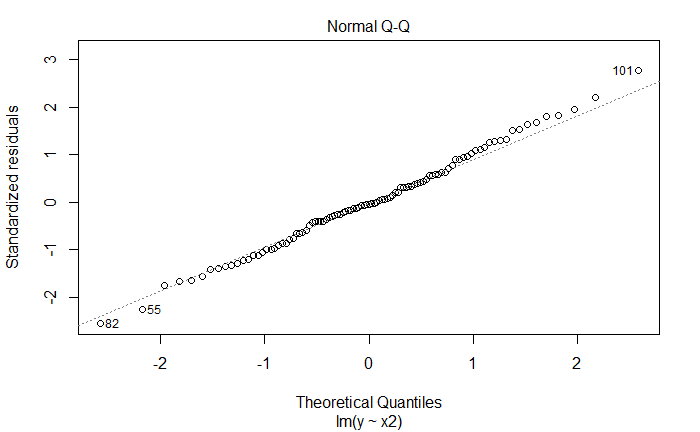

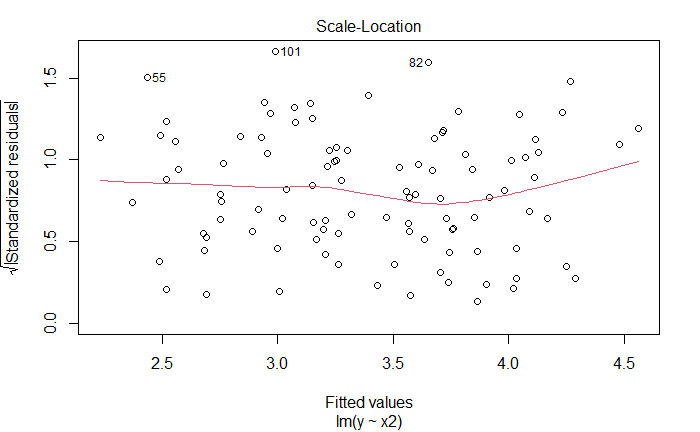

plot(lm_fit_v2)

新增观测是离群点,也是高杠杆点

单变量

y 对 x1

lm_fit_x1_v2 <- lm(y ~ x1)

summary(lm_fit_x1_v2)

Call:

lm(formula = y ~ x1)

Residuals:

Min 1Q Median 3Q Max

-2.8899 -0.6553 -0.0917 0.5679 3.4070

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.4005 0.2378 10.09 < 2e-16 ***

x1 1.9251 0.4104 4.69 8.74e-06 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.106 on 99 degrees of freedom

Multiple R-squared: 0.1818, Adjusted R-squared: 0.1736

F-statistic: 22 on 1 and 99 DF, p-value: 8.744e-06

plot(lm_fit_x1_v2)

新增观测是离群点,也是高杠杆点

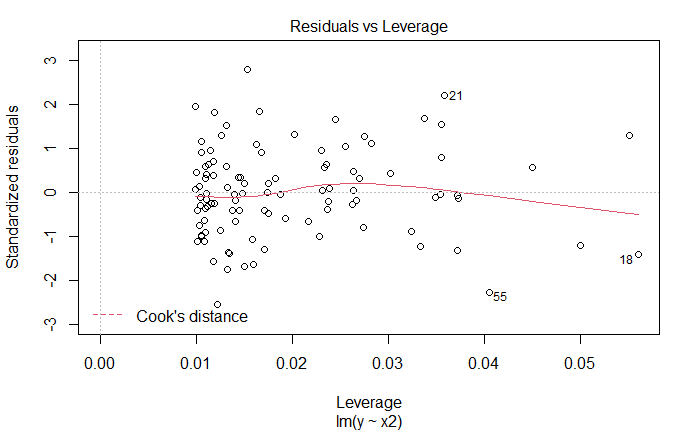

y 对 x2

lm_fit_x2_v2 <- lm(y ~ x2)

summary(lm_fit_x2_v2)

Call:

lm(formula = y ~ x2)

Residuals:

Min 1Q Median 3Q Max

-2.76917 -0.70920 -0.04555 0.64028 3.01186

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.4877 0.3964 3.753 0.000295 ***

x2 1.8755 0.3760 4.989 2.6e-06 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.093 on 99 degrees of freedom

Multiple R-squared: 0.2009, Adjusted R-squared: 0.1928

F-statistic: 24.89 on 1 and 99 DF, p-value: 2.601e-06

plot(lm_fit_x2_v2)

新增观测是离群点,但不是高杠杆点

参考

https://github.com/perillaroc/islr-study

ISLR实验系列文章

线性回归

分类

重抽样方法

线性模型选择与正则化